The Human Impact: How RBI Policies Shape Real Estate in India

Summary

RBI policies in 2025 significantly impact Indian real estate, shaping affordability and investor confidence. Rate changes affect homebuyers' dreams and financial well-being, highlighting the human side of economic policy. Understanding these policies empowers informed decisions.

For countless Indian families, owning a home is more than a financial goal—it is the culmination of dreams, sacrifices, and hope for a better future. Every interest rate change, every RBI announcement, carries weighty consequences: it can bring joy or anxiety, security or delay. In 2025, RBI policies—from repo rate adjustments to credit regulations—are shaping not just markets, but lives. For Meera and Raj, saving for their first apartment in Bengaluru, a small rate cut could mean stepping into their dream home; a hike could stretch their EMIs beyond comfort.

RBI policies touch emotions, security, and life aspirations as much as finances.

How RBI Policies Affect Homebuyers

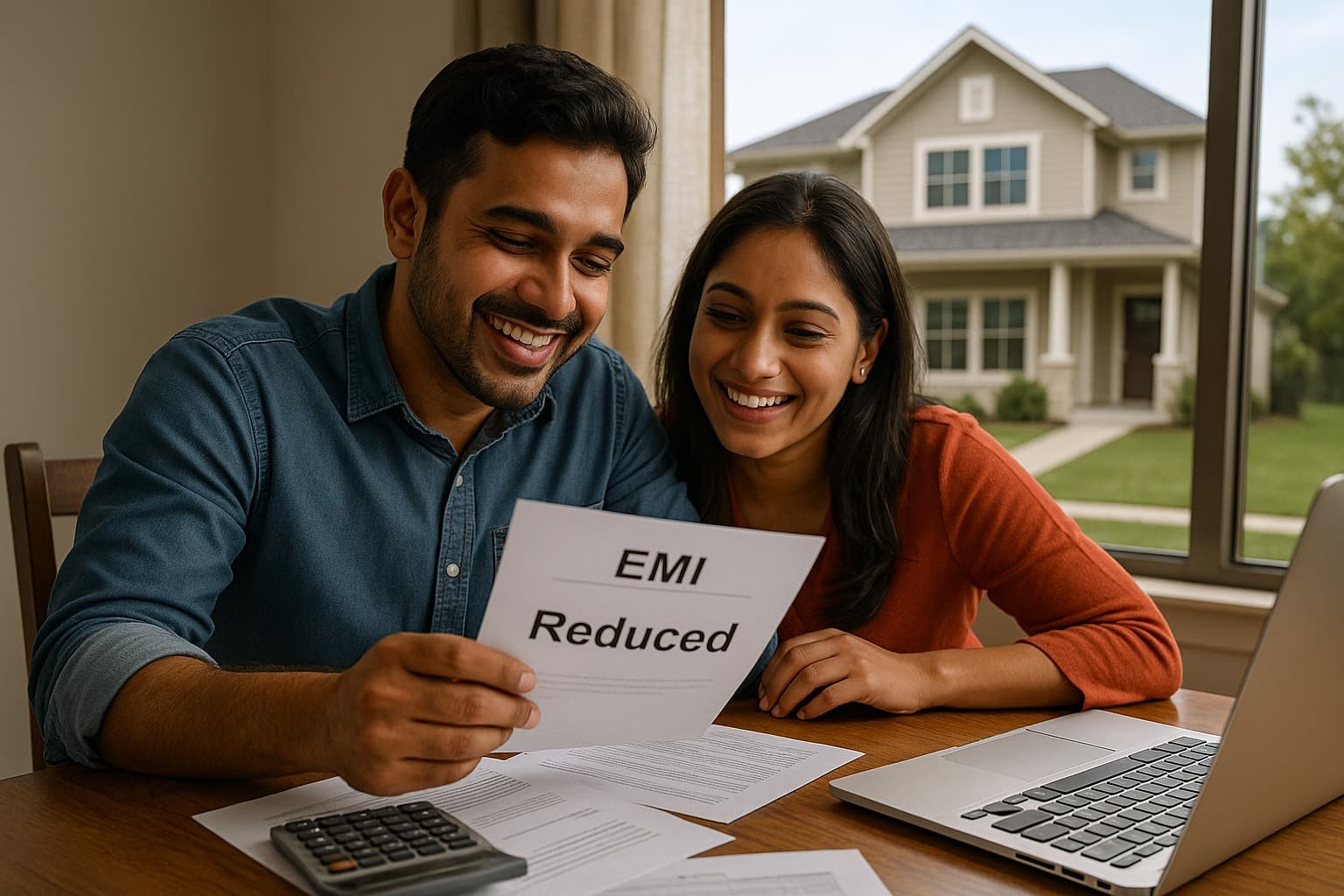

The repo rate, reverse repo rate, and other RBI tools directly influence home loan affordability. When rates decrease, families feel hope: EMIs shrink, making the dream home attainable.

Take Nisha, a teacher in Pune. A recent repo rate cut lowered her monthly EMI by thousands, transforming her long-cherished dream into reality. The emotional relief was immense—years of savings, planning, and anticipation suddenly materialized into her own home.

Conversely, rate hikes can trigger anxiety. For families already stretching budgets, higher EMIs can delay purchases, forcing them to compromise on size, location, or amenities. RBI policies are therefore not just abstract numbers—they affect daily lives, peace of mind, and long-term planning.

Key Impacts of RBI Policies in 2025

1. Repo Rate Cuts

Lower rates reduce borrowing costs, allowing first-time buyers to step confidently into homeownership. Families experience tangible relief and renewed hope.

2. Tightened Credit Norms

Stricter lending rules may slow property purchases. Homebuyers may face emotional stress as life-changing dreams face temporary roadblocks.

3. Inflation Control Measures

Policies controlling inflation influence construction costs. Developers may adjust pricing, indirectly affecting buyers’ affordability.

4. Policy Transparency

Clear, timely communication of policies instills confidence. Families and investors feel secure making financial and emotional decisions in a stable environment.

Real-Life Stories

Consider Aarav, a young IT professional in Bengaluru. He had been planning to buy his first home for years. A repo rate reduction suddenly made EMIs manageable, turning uncertainty into excitement. The joy of holding the keys to his own apartment was an emotional milestone, a reward for perseverance.

Priya, a landlord in Hyderabad, monitors RBI updates closely. Changes affect her financing, property purchases, and investment strategy. For her, policies determine both financial security and peace of mind.

These stories show how RBI policies are deeply human, influencing lives, aspirations, and emotional well-being.

Market Outlook

Analysts predict that RBI actions in 2025 will shape the market significantly:

Repo rate cuts could accelerate housing demand among first-time buyers.

Interest rate hikes may temper speculative buying, ensuring sustainable growth.

Consistent policy communication boosts investor confidence, encouraging new property transactions.

Homebuyers feel hope or stress based on rate movements, while investors adjust strategies for optimal returns. The emotional impact is as real as the financial one.

Strategies for Buyers and Investors

For Homebuyers:

Track repo rate changes and loan interest trends.

Time property purchases to benefit from lower EMIs.

Consider inflation trends affecting construction costs.

Factor policy shifts into long-term financial and emotional planning.

For Investors:

Monitor RBI announcements to identify strategic investment opportunities.

Diversify property investments across metros and Tier-2 cities.

Leverage rate cuts to refinance and improve rental yield.

Balance financial calculations with human insights—tenants’ ability to pay EMIs matters emotionally and economically.

Understanding RBI policies empowers both financial decisions and emotional confidence.

Emotional Perspective

RBI policies influence more than numbers—they affect hope, peace of mind, and life milestones. For first-time buyers, rate cuts can transform dreams into tangible homes. For families, they provide security; for investors, clarity and confidence.

The emotional journey tied to these policies is immense: relief, pride, stress, and anticipation all intertwine. Every decision to buy, borrow, or invest carries emotional weight, reminding us that real estate is as human as it is financial.

Final Thoughts

The impact of RBI policies on real estate in 2025 extends far beyond interest rates. It shapes affordability, housing demand, and investor confidence, but most importantly, it touches human lives. A small rate change can enable a family to move into their first home; a tighter credit norm can temporarily delay cherished dreams. Understanding these policies helps buyers and investors make informed decisions, balancing numbers with emotion, and ensuring that financial strategies align with life goals and emotional fulfillment.

Summary (100 words)

RBI policies in 2025 influence India’s real estate deeply, affecting interest rates, home loan affordability, and investor confidence. Rate cuts can turn long-saved dreams of homeownership into reality, bringing relief, pride, and emotional fulfillment. Conversely, higher rates or tighter credit rules can delay purchases, creating stress and uncertainty. Families, young professionals, and landlords all experience the human impact of these decisions. Real-life examples of first-time buyers and investors highlight how RBI actions shape not just financial outcomes, but life milestones and emotional well-being. In 2025, RBI policies remain a critical factor in both the economic and emotional journey of real estate.